SaaS M&A Volumes and Valuations

“2024 Review and 2025 Predictions”

SaaS M&A Volumes and Valuations

“2024 Review and 2025 Predictions”

I spend at least 25% of my time researching SaaS M&A trends, focusing on financial performance metrics, go-to-market strategies, and consolidation patterns. Below is a summary of 2024 SaaS M&A activity, including transaction volumes, valuation trends, and the most active buyers—followed by my predictions for 2025 and key recommendations for SaaS companies preparing for acquisition.

2024 SaaS M&A Activity

M&A volume in the SaaS industry increased slightly in 2024, with 2,107 transactions, slightly up from the 2,095 transactions in 2023.

Overall software M&A activity rose 2.7%, reaching 3,452 total transactions.

Despite stabilizing interest rates, the expected higher surge in M&A activity did not materialize due to:

Higher customer acquisition costs for smaller SaaS point solutions

A tougher funding environment for legacy SaaS companies with weaker growth or unit economics

Private equity firms seeking consolidation opportunities, particularly in saturated markets

Below is a chart highlighting the past ten years of SaaS M&A activity:

SaaS M&A Activity (2015 - 2024)

Source: SEG 2025 M&A Report

2024 SaaS M&A Valuation Trends

SaaS M&A valuations showed signs of recovery, particularly in Q4 2024:

Enterprise Value (EV) to Revenue Multiples:

2021: 6.4x

2022: 5.2x (-20% YoY)

2023: 3.8x (-27% YoY)

2024: 4.1x (+8% YoY)

Q4 2024 Valuations Showed Positive Momentum:

Mean EV/Revenue multiples increased 19% to 6.0x in Q4

Public SaaS market rebound in late 2024 boosted confidence

Source: SEG 2025 M&A Report

Source: SEG 2025 M&A Report

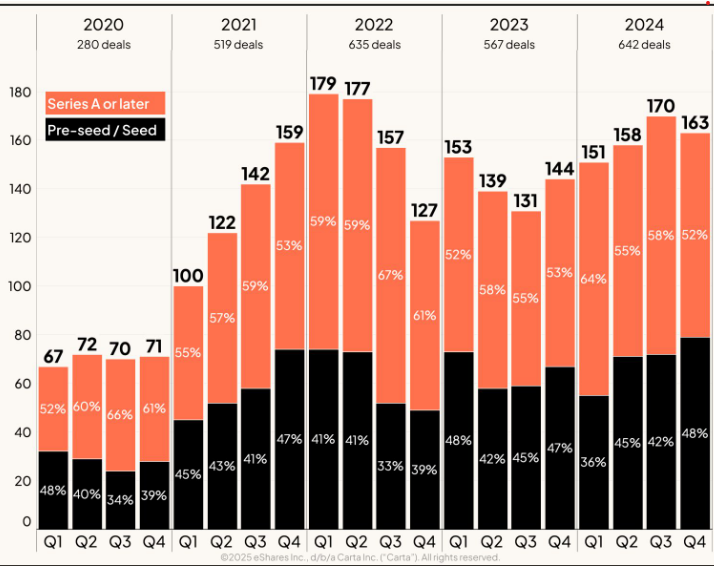

Early Stage Companies Represent a Material Share of M&A Volume

Peter Walker, Head of Insights at Carta is one of my favorite sources for all things private, start-up company equity, valuations and trends. He recently shared a chart that highlighted that ~45% of private, start-up company acquisitions were of pre-seed and seed companies in 2024.

The below chart - though not limited purely to SaaS companies highlights the details:

Source: Peter Walker, Carta

Private Equity (PE) and Strategic Buyers in 2024

Private equity firms continued to lead SaaS acquisition activity in 2024, accounting for 57% of deals, while strategic buyers represented 42%.

Source: SEG 2025 M&A Report

Most Active Private Equity Buyers (# of transactions)

Main Capital Partners (9)

KKR (7)

EQT (6)

TA Associates (5)

Bain Capital (5)

Thoma Bravo (4)

Accel-KKR (4)

Vista Equity (3)

Most Active Strategic Buyers (# of transactions)

Valsoft (14)

Constellation Software (12)

Access (7)

Visma (7)

ServiceNow (6)

Accenture (5)

Cloudflare (5)

Descartes (5)

2025 SaaS M&A Predictions and Recommendations

M&A activity will accelerate in early 2025 as stabilizing interest rates and significant dry powder in private equity lead to a wave of acquisitions.

1️⃣ SaaS M&A Volume Will Increase

A revived IPO market, including 80+ IPO-ready SaaS companies will boost confidence in private company acquirers

PE firms will increase debt leverage and SaaS acquisitions as credit markets stabilize

AI-native SaaS companies will command the highest multiples

2️⃣ Valuation Multiples Will be Materially Influenced by Size, Growth Rate & AI Capabilities

AI-native companies: 8x-12x EV/Revenue multiples

Mid-market SaaS deals ($250M - $1B): 3x-8x multiples

Low-end SaaS deals (<$250M): 2x-3.5x multiples, unless top-quartile performance metrics drive a premium

3️⃣ Private Equity Will Lead M&A Volume - Especially in $1B+ Valuations

PE buyers will increase focus on EBITDA multiples, not just revenue multiples

Consolidation plays and platform expansions will drive SaaS acquisitions

Expect greater leverage in PE-backed SaaS deals

4️⃣ Strategic Buyers Will Prioritize Customer Expansion and AI Opportunities

Public SaaS companies will target acquisitions that expand cross-sell/upsell opportunities into their existing customer base

Companies with large amounts of customer data that can leverage the power of AI and strong distribution will be attractive acquisition targets

AI-native companies will continue to be attractive targets for legacy SaaS and VC alike

How SaaS Companies Can Prepare for M&A in 2025

✅ Optimize Key Financial Metrics

Growth & Efficiency: NRR, GRR, CAC Ratio, Payback Period, Rule of 40

Profitability: EBITDA margins, Customer Lifetime Value to CAC Ratio

Valuation Readiness: Be prepared for PE firms to focus on EBITDA multiples and strategic buyers to focus on EV/Revenue multiples

✅ Positioning for Different Buyer Types

For PE Buyers: EBITDA and debt capacity will be key

For Strategic Buyers: Customer retention, cross-sell potential, existing customer data and AI integration will drive premiums

✅ Demonstrate Product Stickiness

Show consistent and increasing product utilization trends - a leading indicator of retention and lifetime value

If using usage-based pricing, clearly separate committed ARR vs. variable ARR

✅ Leverage Industry Benchmarks and Reports

Compare financials against:

Bain & Company’s “State of Private Equity in SaaS” presented at SaaS Metrics Palooza

Final Takeaways

📈 SaaS M&A activity will gain momentum in 2025, driven by stabilizing interest rates, PE firms deploying dry powder and often - necessity

📊 AI-native companies will command premium multiples, but legacy SaaS valuation multiples will be greatly affected based on growth rate, customer retention and financial efficiency

💰 PE buyers will place a higher priority on EBITDA, while strategic buyers will prioritize customer retention, cross-sell opportunities, and AI leverage

🚀 SaaS companies should proactively align financial metrics with buyer expectations to maximize valuation potential

If you would like to receive early access to the latest Billing Model and Pricing Process Benchmarks Research Report based upon our original research conducted with Maxio - click here to download the report and gain free access to the interactive portal where the findings are available to be viewed by company attributes specific to your company!